By now, stories of the travesty at Camp Lejeune have spread throughout the nation. People across many different states are aware of the unforgivable contamination that took place at this military base, and countless lives have been changed forever. Many family members are still grieving the loss of their loved ones – losses that could have been prevented if things had been handled differently. Perhaps you are just learning about the Camp Lejeune contamination for the first time.

Maybe you are well aware of the contamination, and you are searching for additional answers. Perhaps you have suffered an injury after being exposed to toxic chemicals at this military base, and you are ready to file a lawsuit. Or maybe you have lost a family member, and you want to file a wrongful death lawsuit on their behalf.

Alert: We have created “The Complete Guide to Camp Lejeune Water Contamination Lawsuits” You can get a general overview in this article, or See the Complete Guide Here.

Whatever the case may be, an experienced personal injury attorney can help you strive for the best possible results. During an initial consultation, your attorney can assess your unique situation and determine the best route forward. From there, you can work toward a fair financial settlement that covers your full range of damages. These might include medical expenses, missed wages, psychological trauma, funeral expenses, loss of consortium, and many others. Due to the statute of limitations, it always makes sense to book your consultation as soon as possible. If you delay for too long, you may lose the opportunity to sue altogether.

What Happened at Camp Lejeune?

While there is plenty of news about Camp Lejeune lawsuits, it is surprisingly difficult to find out what actually happened at this military installation. Over more than 30 years, from 1953 to 1988, Marine Corps Base Camp Lejeune exposed its soldiers to extremely toxic water. In fact, the water contained 280 times the standard safety limits for known carcinogens. Not only did the soldiers drink the water on a regular basis, but they also bathed in it and cooked with it constantly. Even though the Navy set out strict water supply standards prior to the exposure, these guidelines were completely ignored by high-ranking staff at Camp Lejeune.

These chemicals included:

- Industrial solvents

- Benzene (a known carcinogen)

- PCE (perchloroethylene or tetrachloroethylene)

- TCE (trichloroethylene)

- TCE degradation products trans-1,2-DCE (t-1,2-dichloroethylene)

- Vinyl chloride

So, where did all these chemicals come from? According to the CDC, the main source of the contamination was a company called ABC One-Hour Cleaners – an off-base dry cleaning operation that was dumping its waste near the Tarawa Terrace water treatment plant. The Hadnot Point water treatment plant was also contaminated by TCE degradation products. These degradation products were tracked to several sources, including leaking underground storage tanks, industrial area spills, and waste disposal sites.

Both of these water treatment plants were reportedly shut down in 1985 – but by that time, the damage had already been done. The CDC lists several potential adverse medical effects of the contamination, including:

- Kidney cancer

- Multiple myeloma

- Leukemia

- Adverse birth outcomes

- Aplastic anemia and myelodysplastic syndromes

- Bladder cancer

- Liver cancer

- Non-Hodgkin’s lymphoma

- Parkinson’s disease

- Fetal death

- Eye defects

- Low birth weight

- Chronal atresia

- Major malformations

- Miscarriage

- Neural tube defects

- Oral cleft defects (including cleft lip)

- Breast cancer

- Cervical cancer

- Ovarian cancer

- Prostate cancer

- Rectal cancer

- Impaired immune system function

- Neurological effects

- Severe, generalized hypersensitivity skin disorder

In addition, the US Department of Veterans Affairs lists a number of “qualifying health conditions” for those seeking compensation, including:

- Esophageal cancer

- Breast cancer

- Renal toxicity

- Female infertility

- Scleroderma

- Lung cancer

- Hepatic steatosis

- Miscarriage

- Neurobehavioral effects

Simply listing medical conditions and chemicals does not paint the full story. A much more personal account was described by one family member in an article published in MarineTimes. This article described how the author (a retired Master Sgt.) had lost his daughter due to the toxic water in Camp Lejeune. During his 12-year stay at the camp, he conceived a daughter. The mother also lived there and consumed the toxic water without realizing it during her pregnancy. The child only reached the age of nine before she died of leukemia. The author stresses that there is no family history of cancer in either the mother or the father, and the assumption is that the death must have been caused by Camp Lejeune’s toxic water.

The author goes on to say that his daughter’s passing was never acknowledged by the US government or military – and his family has never been compensated. Recently, a 2016 court opinion prevented affected families from taking legal action, with the government relying on sovereign immunity to shield themselves from lawsuits. This was despite the fact that the DHHS openly acknowledged the fact that the toxic water increased the risk of cancer and other health issues.

The Camp Lejeune Justice Act (PACTA Act)

On August 10th, President Joe Biden signed the PACTA Act into law. This veterans’ healthcare and benefits bill also contained the Camp Lejeune Justice Act, which finally removed legal roadblocks for families and service members who had been harmed by the toxic water. Almost immediately, 5,000 claims were filed – and some believe that this could represent the largest mass litigation in US history. The Camp Lejeune Justice Act specifically provides an exception to sovereign immunity, allowing plaintiffs to file their claims through the Eastern District of North Carolina.

The main takeaway is that injured veterans are set to receive billions of dollars in compensation for various issues. $300 billion has been set aside for things like burn pit smoke in Afghanistan, Agent Orange in Vietnam, and of course, toxic water at Camp Lejeune.

At the same time, hundreds of thousands of injured soldiers are also suing 3M for deficient earplugs – but the Camp Lejuene mass tort could go even further. In fact, the DHHS’ Agency for Toxic Substances and Disease Registry believes that as many as one million people were affected by the toxic water, and some attorneys attached to the litigation believe 500,000 people could eventually decide to file claims. If this is true, the Camp Lejeune mass tort will indeed outdo the 3M lawsuit.

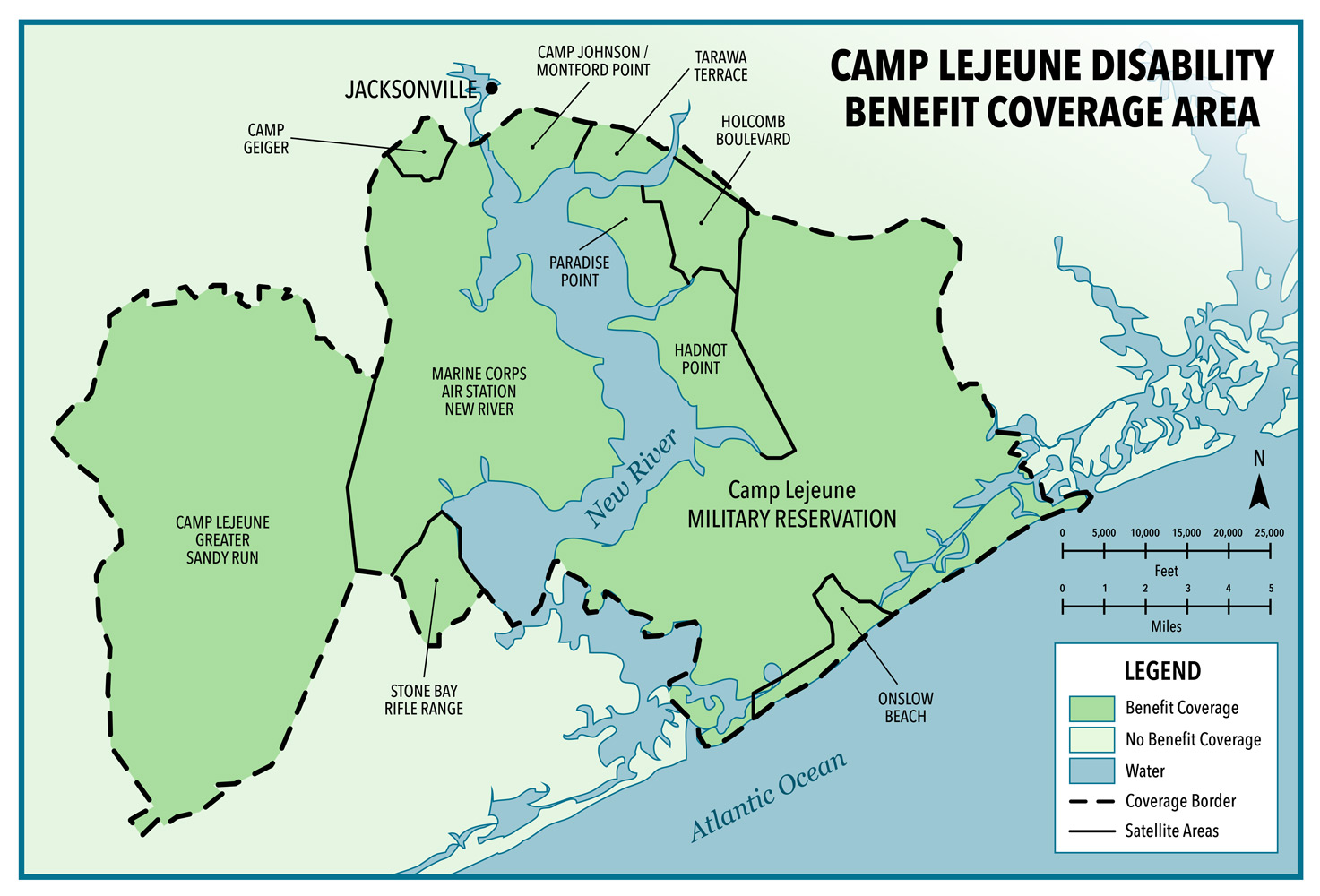

But what are the details of the Camp Lejeune Justice Act? It lays out a number of circumstances that must be present before you can file a claim. First of all, you need to have lived in the area during a period stretching from 1953 to 1988. As you may know, the base itself is close to Jacksonville. However, those who lived in Jacksonville during this period are not eligible for compensation. The affected area ranges from Camp Lejeune Greater Sandy Run in the west to Holcomb Boulevard and the Camp Lejeune Military Reservation in the East.

The southernmost affected areas are Onslow Beach and Stone Bay Rifle Range, while the northernmost affected areas are Camp Geiger, Camp Johnson, and Tarawa Terrace. If you served in the camp, you probably spent time in many of the affected areas. A map is available here. While most of the people filing claims will be past or present US military service members, you may also sue if you were simply living near the affected area without being connected to the military.

Another condition is that you can only file your lawsuit within a two-year period. This means that it is important to get in touch with an experienced personal injury attorney as soon as possible if you have been affected by this travesty. This two-year period is often referred to as a “lookback window,” and once it expires, you will lose the right to file a claim.

If you want to file a claim through the VA for disability benefits, you must have served at Camp Lejeune for at least 30 cumulative days. Alternatively, you can file a claim if you served for 30 cumulative days at MCAS New River. In addition, you can only file a claim through the VA if you did not receive a dishonorable discharge. Veterans, reservists, and guardsmen are all covered under the VA. That being said, it is worth noting that filing a claim for VA disability benefits is not the same as filing a claim against the US government.

Another crucial detail is that you can still file for compensation even if you have already received health benefits from the Veterans Administration in connection with chemical exposure at Camp Lejeune. Even though your medical bills may have been paid, you can still receive compensation for non-economic damages, such as emotional distress, loss of quality of life, or pain and suffering.

Past Issues With Camp Lejeune Claims

Even though this mass tort has the potential to become the largest of its kind in US history, this does not mean that the process will be smooth. In fact, past experiences tell us that affected individuals may experience considerable issues as they attempt to get compensation for their injuries at Camp Lejeune. People have been filing claims with the VA since approximately 2012, and many of these individuals have experienced notable roadblocks along the way.

According to the Marine Corps Times, there is a real chance that injured individuals may “never see a dime.” A representative from Disabled American Veterans warned that individuals should do their fair share of research before filing a lawsuit to avoid unnecessary legal costs. Many advocates are cautious, promoting a “wait and see” approach as the VA goes through 150 pages of legislation and publishes new regulations. We’re still not quite sure whether veterans who win these lawsuits will lose their existing disability and health care benefits with the VA. Some have pointed out that when you add attorney fees into the mix, this could result in a net loss that outweighs any potential gain.

Of course, you can discuss these concerns alongside a qualified, experienced personal injury attorney before you take legal action. The best lawyers are honest and impartial, providing legal advice that genuinely serves your best interests. The good news is that the VA has publicly stated that it will not deny your pending disability claims or cut you off from existing services if you simply file a lawsuit related to the Lejeune Justice Act. What happens if you win? That’s another question altogether, and the VA recently announced that:

“Any award must be offset by the amounts of VA benefits provided in connection with health care or disability relating to exposure to the water at Camp Lejeune.”

Remember, your lawsuit could take years to complete. Assuming you win your lawsuit, you may only start receiving payments by 2024. Of course, these are all topics you can discuss with your lawyer, who can help you weigh up the pros and cons of filing a lawsuit. One thing’s for sure: the potential payout from a successful lawsuit can certainly outweigh any financial assistance you are currently receiving from the VA or any other government agency.

Another major issue involves the mishandling of Lejeune water claims by the VA, which reportedly resulted in $14 million of lost compensation for victims. According to Military.com, the Department of Veterans Affairs mishandled a staggering 40% of all disability claims filed in relation to contaminated water issues at Camp Lejeune. This not only resulted in financial losses but also delayed benefits for those who were desperately waiting for assistance.

Apparently, the VA simply flat-out denied 17,200 claims without explaining why. The organization also failed to ask for additional information. Another 2,300 veterans failed to receive compensation because they were assigned incorrect dates, resulting in a total of $14 million in denied retroactive payments. 1,500 additional claims were denied due to unspecified “technical issues.”

These worrying developments highlight the need to work with a qualified, experienced personal injury attorney as you approach your claim. With help from one of these legal professionals, you can overcome any hurdles you may face and get ahold of your compensation without unnecessary delays.

What Kind of Evidence Do I Need When Filing My Camp Lejeune Claim?

If you are serious about filing a lawsuit for medical issues related to toxic water exposure at Camp Lejeune, you will need to gather evidence. First of all, you will need to prove that you were actually stationed at the base during the period of contamination. The most obvious choice is to provide your military records, which will clearly prove that you were indeed living on MCAS New River or Camp Lejeune during the period of contamination.

The second requirement is to prove that you actually suffered an injury that can be attributed to the toxic water at the camp. This step is perhaps a little more difficult, as it requires you to establish a causal link between your injury and your exposure to the toxic water. This becomes increasingly difficult if many years have passed. In other words, simply living on the base during a time of toxic contamination may not be enough. You will also need to provide medical records showing that you suffered an injury.

And it cannot be just any injury, either. It must be related to the specific chemicals found in the water supply. These may include the range of cancers and other illnesses listed earlier in this article.

If you are filing on behalf of a deceased loved one, locating these medical records could be a challenge. Things would be even more difficult if your loved one refused medical treatment, as it then becomes challenging to link their passing to their time at the camp.

If you are unsure of what kind of evidence you need, the VA requirements represent a solid reference point. If you have the necessary evidence to successfully file a claim with the VA for your exposure to the contaminated water, you will likely have enough evidence to file (and win) a lawsuit. Of course, your attorney can certainly help you locate, compile, and present the necessary evidence as you pursue legal action.

Enlist the Help of a Qualified Attorney Today

If you’ve been searching for a qualified, experienced personal injury attorney, look no further than National Security Law Firm. We know that exposure to toxic chemicals can cause tragic, life-altering, and terrible injuries.

We’re ready to help you fight for your rights. Make no mistake – you are fully entitled to fight for your rights and pursue a fair, adequate level of compensation for everything you’ve been forced to endure. While internet research may be a positive first step, it cannot replace real, targeted advice from a qualified lawyer. Book your consultation today, and we can get you started with an effective action plan right away.

Sources

- https://www.va.gov/disability/eligibility/hazardous-materials-exposure/camp-lejeune-water-contamination/

- https://www.publichealth.va.gov/exposures/camp-lejeune/

- https://www.reuters.com/legal/government/camp-lejeune-water-contamination-claims-total-about-5000-so-far-us-navy-says-2022-09-12/

- https://www.marinecorpstimes.com/news/pentagon-congress/2022/08/18/dont-expect-quick-payouts-from-camp-lejeune-water-lawsuits/

- https://www.military.com/daily-news/2022/08/26/veterans-were-denied-14-million-payments-because-va-mishandled-lejeune-water-claims.html

With nearly 20 years of experience representing injury victims, the team of attorneys at Hicks Law Firm in Costa Mesa has seen a thing or two. As you purchase school supplies, get those last-minute haircuts, and stock up on school snacks and juice boxes, be sure to also carve out time to review our top back-to-school safety tips, so you and your family can have a safe and successful back-to-school season.

With nearly 20 years of experience representing injury victims, the team of attorneys at Hicks Law Firm in Costa Mesa has seen a thing or two. As you purchase school supplies, get those last-minute haircuts, and stock up on school snacks and juice boxes, be sure to also carve out time to review our top back-to-school safety tips, so you and your family can have a safe and successful back-to-school season. Always walk young children to the bus stop and stay with them until the bus arrives. Older children may be able to walk to the bus by themselves, but only if the road and walkway permit them to do so safely. If the path to the bus does not have a wide sidewalk and especially if it had tight turns that a driver or pedestrian cannot see around very well, it might not be a safe route for your child to walk alone.

Always walk young children to the bus stop and stay with them until the bus arrives. Older children may be able to walk to the bus by themselves, but only if the road and walkway permit them to do so safely. If the path to the bus does not have a wide sidewalk and especially if it had tight turns that a driver or pedestrian cannot see around very well, it might not be a safe route for your child to walk alone.

If you

If you  At Hobson & Hobson, P.C., our

At Hobson & Hobson, P.C., our

")

{kind=link}